The difference between KYC & AML?

2022-07-18

Recommend Articles

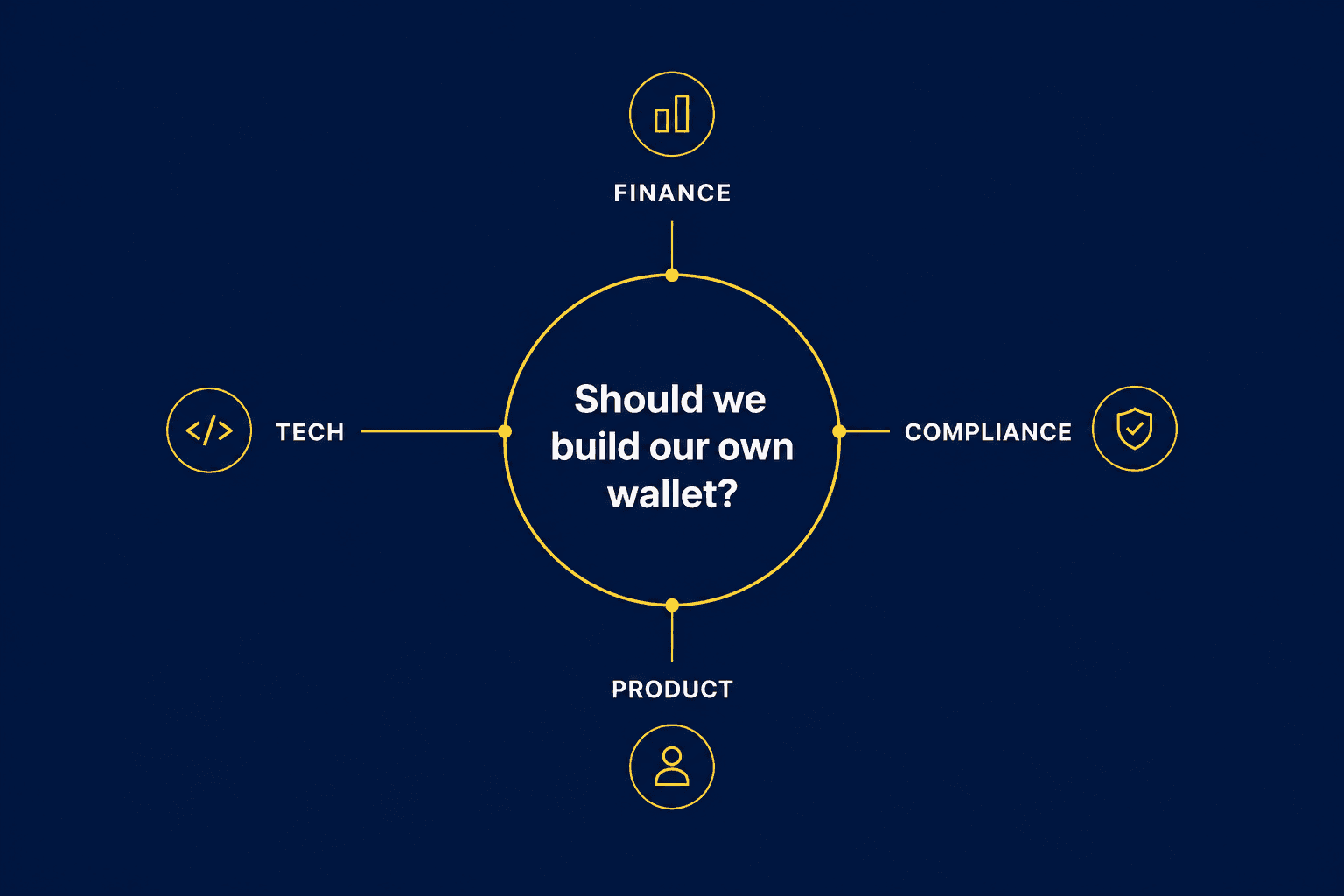

Where White-Label Wallet Projects Actually Get Stuck

How Mining Farms Use Stablecoins for Electricity Payments: From Collection to Compliance

What Are KYC, KYB, and KYA? What Businesses Actually Need to Check When Using Virtual Assets

Hot Articles

From 2,000 BTC to Enterprise Treasury Risk

Hot Tags

HotNewsNFTBlockchainDeFiSecurityComplianceUpdates